What is the IFI?

The real estate wealth tax (IFI) applies only to taxpayers’ non-professional real estate assets and “paper stones” (SCPI, OPCI).

This is a declaratory tax, paid by individuals whose net taxable real estate assets on January 1 of each year are worth €1.3 million or more.

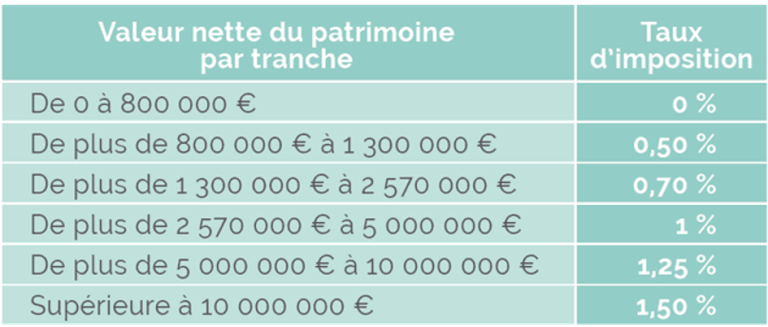

Taxation applies to the value of assets in excess of €800,000 according to the following progressive scale:

How do I file my IFI tax return?

If your real estate assets exceed €1.3 million, you now have to declare your wealth tax (IFI) at the same time as your annual tax return.

All you need to do is specify the composition of your net taxable real estate assets in the attached documents. As a general rule, you are not required to enclose supporting documents, but it is important to keep them on hand for the tax authorities. The tax authorities may ask you at any time for the documents needed to justify the composition or valuation of your assets on January 1 of each year.

When you file your IFI tax return, indicate the amount of your donation in box 9NC of the 2042-IFI tax form. The Inserm Foundation will send you a tax receipt, which you should keep in case of a request from the tax authorities.

What assets must be declared for the IFI?

Your wealth tax return (IFI) must include all the real estate in your estate portfolio, including your principal residence, even if a 30% discount applies to the latter.

All other properties – second homes, leased properties, etc. – must be included in your IFI return. – must be included in your IFI return, with the exception of real estate used for professional purposes.

The law provides for the exemption from taxation of certain assets, notably business assets, such as those used in the operation of a company that owns these assets, or those used in the taxpayer’s main business, even if this is carried out on an individual basis.

What is the deadline for making an IFI-deductible donation?

The dates for declaring your real estate tax (IFI) are now the same as those for your income tax (IR). Your IFI return should therefore be sent in at the same time as your IR return, in the spring (the dates have not yet been set).

How to reduce your IFI?

By making a donation to the Inserm Foundation, you can benefit from a tax reduction of 75% of the amount donated on your Impôt sur la Fortune Immobilière (IFI), up to a limit of €50,000 per year.

Info

To calculate the amount of your donation and reduce your IFI to zero, here’s the formula to use:

Amount of your donation = IFI/0.75

A commitment to research

Your donation helps finance innovative scientific projects and support researchers engaged in the fight against disease. By contributing to the Inserm Foundation, you play an active role in health advances and in improving tomorrow’s healthcare.

Can I benefit from both an IFI reduction and an IR reduction?

Yes, it is possible to split a donation between these two tax schemes. Once the deduction limit for the Impôt sur la Fortune Immobilière (IFI) has been reached, the excess amount can be deducted from the Impôt sur le Revenu (IR), up to a limit of 20% of net taxable income, and can be carried forward for up to five years.

To optimize your tax return, it is advisable to make two separate donations in order to obtain two tax receipts. If you lose one of them, you can request a duplicate from the Donor Relations Department.

How do I make an IFI donation?

- Online: via a secure form on the Inserm Foundation website.

- By cheque: by sending your donation to Relation Donateurs – Fondation Inserm: 2 – 10 rue d’Oradour-sur-glane – 75015 Paris

- By bank transfer: by contacting the Foundation on 07 64 43 23 64 or by e-mail at fondation.contact@inserm.fr